Status: DG1

Author: Llama

Created: 2021-07-06

Requires: IIP-58: Launching Pulse Aggregate Yield (PAY)

Simple Summary

Llama would like to partner with Index Coop (IC) to co-manage the Llama Diversified Index strategy. The Llama Diversified Index (LDI) is a productive and diversified crypto index that optimizes returns relative to risk across various sub-asset classes within the crypto ecosystem.

LDI has already secured approximately $3.5M of external funding. Llama is acutely aware of limited dev resourcing within DeFi and is willing to share the dev workload associated with developing and maintaining LDI. Llama would also like to highlight the 15% allocation to the Pulse Aggregate Yield index (PAY) within LDI.

Llama is truly excited by the prospect of partnering with Index Coop and looks forward to developing a long-term prosperous relationship.

Motivation

This new set has been developed to provide holders a diversified portfolio of productive assets wherever possible to maximise returns. By providing holders with an automated diversified asset allocation solution, LDI enables passive investment in a diversified set that provides access to the main thematic investment sectors on the Ethereum network. The diversified portfolio construction has already proven to have strong product market fit as Gitcoin has expressed interest in becoming an early investor in the product.

In time, LDI will be integrated across DeFi, allowing for extrinsically productivite opportunities to be generated on top of a balanced index, further enhancing the appeal of holding a diversified portfolio. Llama has built an extensive network across DeFi and is able to accelerate LDI integrations across the ecosystem. At the time of writing, Llama has approximately 25 contributors that are also members of other DeFi communities.

LDI has several key advantages over traditional diversified portfolios:

- Utilization of productive assets where possible.

- A more sophisticated asset allocation methodology that optimizes for Sharpe ratio while integrating appropriate constraints to ensure diversification among established crypto sub-asset classes.

- Low vol USD yield aggregation (PAY)

- Access to a liquid secondary DEX market

- LDI productive use cases

Llama has already received expressions of interest from various parties regarding this particular product and intends to create complementary products as part of our overall treasury management strategy solutions.

Size of Opportunity

DeFi treasuries have amassed a total AUM of over $6B. As DAOs seek to diversify their treasuries, passive and diversified portfolio solutions will enable simplified management. The total addressable market for a diversified Ethereum-focused crypto portfolio is tremendous. Capturing a small portion of this overall market means generating significant AUM for Index Coop. A diversified crypto index product currently does not exist within DeFi and therefore represents a unique opportunity for Index Coop to partner with a Treasury Management specialist in Llama.

Llama’s network includes university endowment funds which Llama believes will find LDI attractive. Llama has already discussed the LDI with a number of DAOs and found strong support for the product which can be used as an allocation within a broader treasury management strategy.

Product Differentiation

There are currently no diversified portfolio offerings available as crypto-native structured products that optimize for returns relative to standard deviations among various sub-asset classes. Indices like BED offer simplified solutions for the risk assets within a portfolio, but they do not allocate to stablecoins (an essential component of a diversified crypto strategy). In addition, the methodology of BED equal-weights the sub-asset classes (e.g. Bitcoin, ETH, and DeFi) rather than optimizes risk/reward between them. While there is definitely a market for equal-weighted indices like this, the LDI intends to offer a more sophisticated portfolio management solution.

The introduction of a stablecoin allocation will lead to automatic rebalancing toward risk-on assets during periods of market stress and toward risk-off assets during periods of market euphoria. This diversified approach ensures contrarianism and is a key component of a portfolio management mindset.

Finally, a bias toward productive assets addresses a key treasury diversification goal. For example, Nexus Mutual recently invested a large amount into stETH and Fei Protocol recently approved purchasing stETH. Since this product attempts to create a diversified allocation while also ensuring productivity where possible, there is no need for a DAO treasury seeking a simple, passive solution to do more with their investment assets outside of holding LDI.

Liquidity Analysis

The underlying assets within LDI are all readily available within DeFi as ERC20 tokens. Most tokens can be purchased via Sushiswap, Uniswap, Curve by depositing capital into the respective protocol. For tokens traded via DEXs, there is ample liquidity to facilitate rebalancing when compared to some of the more illiquid components in DPI.

The only token with underlying liquidity concerns is the productive iteration of AAVE. stkAAVE has a lock up period and xToken products like xAAVEa & xAAVEb also rely on AAVE being unstaked periodically to provide unwrapping liquidity. Llama expects at the time of launch xToken will have launched AAVE-xAAVEa & AAVE-xAAVEb pools on Uniswap V3 which are expected to provide sufficient rebalancing liquidity. These contracts are currently being audited.

LDI intends to utilise a combination of Exchange Issuance and on market liquidity to facilitate rebalancing the PAY allocation within LDI.

Methodology

LDI is intended to provide a diversified portfolio of crypto assets across a variety of sub-asset classes. The Index strives to provide an effective portfolio solution for DAO treasuries and individuals alike.

The allocation will initially be divided among 6 sub-asset classes: Stablecoins, Bitcoin, ETH, DeFi, Metaverse, and Web3 Infrastructure. These sub-asset classes were determined by analyzing the current crypto market to identify key themes and differentiated asset types. Sub-asset classes could change over time as new themes and asset types emerge. The reasoning for the current sub-asset class elections are as follows:

- Stablecoins (Target: 15%) - Stablecoins are largely uncorrelated to the broader crypto ecosystem. The stability inherent in stablecoins make them essentially a cash equivalent while offering returns comparable to traditional equities when deployed productively. Having a sizable stablecoin allocation allows for a contrarian investment approach during the rebalancing process: risky assets are trimmed during periods of strong performance and are added to during drawdowns. This rebalancing approach has been shown to outperform the classic buy-and-hold strategy over multiple market cycles.

- Bitcoin (Target: 15%) - Bitcoin has the lowest volatility of the other risky asset types included in the index, serving to bring down total portfolio volatility without sacrificing too much upside. Its fixed supply and position as the largest high-quality crypto asset makes it a kind of safe-haven asset during periods of market instability while displaying characteristics reminiscent of traditional real assets like gold.

- Ether (Target: 35%) - Ether is the life-blood of the Ethereum economy and the main asset used to conduct operations by DAOs outside of their native governance tokens. Since ETH is essentially the money of the ecosystem, it is a primary asset for DAO and individual portfolios. Investing in ETH provides exposure to a variety of crypto themes while also providing a remarkable risk/reward profile versus other crypto assets including Bitcoin.

- DeFi (Target: 20%) - DeFi has emerged as one of the largest opportunities within crypto, and is arguably one of the first killer applications of blockchain technology. There is strong demand for DeFi assets as evidenced by new centralized offerings (e.g., the Bitwise DeFi Index), the success of DPI, and the inclusion of DeFi in the BED meme. In addition, many DAO treasuries have shown interest in acquiring the assets of other DeFi protocols.

- Metaverse (Target: 10%) - The Metaverse is quickly emerging as one of the key themes of the 21st century as we spend an increasingly larger amount of time in digital spaces. The theme has been highlighted in traditional finance, specifically around the Roblox IPO, but NFTs, blockchain gaming, and crypto in general provides a better platform for some of the core tenets of the theme. While the opportunity is still in the early innings, the success in capturing the imaginations of investors thus far warrants an investment in the space.

- Web3 Infrastructure (Target: 5%) - Web3 Infrastructure, including oracles and sub-graphs, have enabled DeFi to flourish. As a sub-asset class, it is expected that middleware remains less correlated to other sub-asset classes like DeFi and the Metaverse as it is more directly tied to the growth of on-chain data.

Llama will periodically review the strategic weightings above to determine if they are still suitable based on market dynamics. The allocation size of each sub-asset class will be determined based on qualitative and quantitative characteristics, including but not limited to potential size of the opportunity, correlation to existing asset classes, investor appetite, long-term viability, and suitability within a treasury portfolio. Llama will maintain a committee within LlamaDAO focused on analyzing current and future sub-asset classes.

The allocation to the underlying constituents of each sub-asset class will follow a risk-optimized market cap weighting methodology outlined below:

- Llama will use a combination of quantitative and qualitative screeners to identify core assets of each sub-asset class to be included. The selection process will seek to identify best-in-class assets that are representative of the sector.

- A fully-diluted market-cap weighted methodology will be used on the screened assets to determine an initial weight. A ‘10.0% of sub-asset class’ band will then be applied around the initial investment allocation to determine the possible tactical allocation range. The maximum allocation for each asset will be limited to 5.0% of the total portfolio to ensure diversification. The minimum allocation will be set at 1.0% of the total portfolio to ensure inclusion justifies the frictional costs associated with rebalancing.

- The final allocation is determined by optimizing for maximum Sharpe ratio (return relative to unit of risk). Better risk/reward assets will be weighted more heavily, while less capital efficient assets will be underweighted relative to the initial market cap weighting within the defined band.

- No leverage or shorting may be used.

Within each sub-asset class, there will be a bias toward productive iterations of each asset.

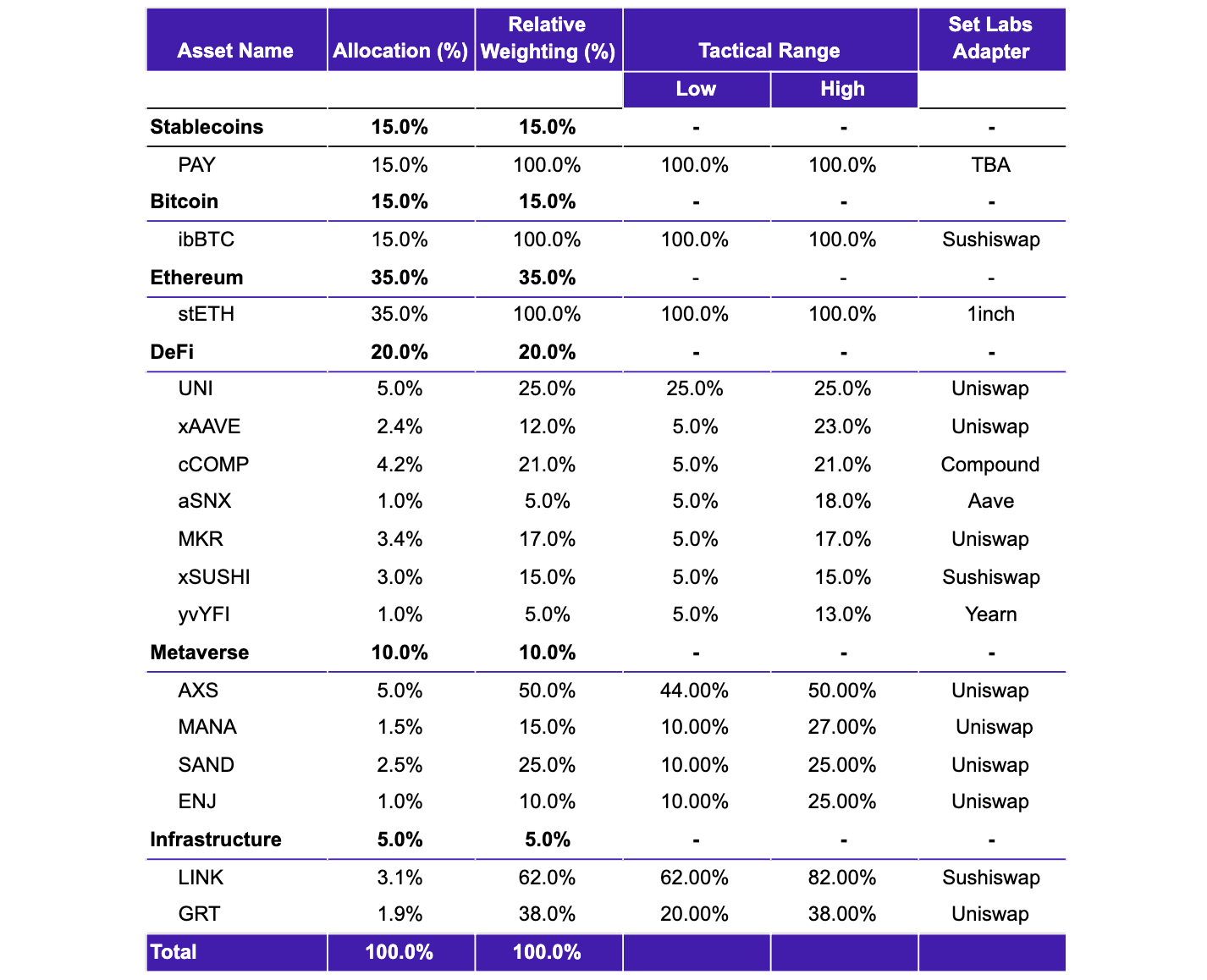

Sample Composition

A sample portfolio composition is shown below. This is subject to change and shall be confirmed prior to launch.

Note:

- TokenSet adapters are shown to indicate relative ease of creating the LDI set

- Issue contracts will require users to deposit wrapped tokens in the correct portions

- Exchange issue function is required

- Exchange issuance shall automate multiple purchases of underlying tokens, minimising slippage and accommodating suitable large trades that would otherwise cause significant slippage in the underlying tokens

- Redemption will release the underlying tokens in the differing proportions

- Productive iterations of underlying assets can vary with time based to optimise returns

Maintenance

Llama will periodically provide Index Coop with an updated LDI composition. Llama is also willing to discuss providing dev resources to assist with the rebalancing process. This can also be extended to include developing any additional adapters that may be required. The prospect of partnering and potentially sharing developer resources symbolises Llama’s commitment to building an alliance within DeFi. LDI = Let’s Do It!

Initial rebalancing frequency is expected to be quarterly. Llama seeks the ability for DAO treasuries to deposit large sums of capital into a contract that acquires the underlying assets gradually over time to minimise slippage. Llama would also like the same functionality built into the redeem function to allow large positions to be unwound over time.

Fee Structure

For Llama and Index Coop to discuss.

Author Background

Llama is building primitives for on-chain treasury management. Llama is working with Aave, Gitcoin, Uniswap, Radicle, ARCx, FWB, and has other top tier DeFi integrations in the pipeline. Llama aims to set the gold standard for DAO treasury management and create category defining templates that apply across DAOs.

Copyright

Copyright and related rights waived via CC0 4.