This is a brain dump I wrote a couple of days ago…

Providing liquidity on DEX whether by individuals or protocols has costs. However, the headline $ value lost can have multiple (overlapping causes):

- Market price exposure

- Impermanent loss on a constant product ratio (xy=K) DEX

- Accelerated IL on uni v3

Market price exposure (for anything other than stable coins).

- In the last 180 days we have seen the following (coingecko spot prices):

- ETH -32%

- INDEX -537

- DPI -50%

- MVI -54%

- DATA -53%

- GMI (since launch 113 days) -62%

So, any portfolio (including POL) constructed from these assets could be expected to have lost 30 to 50% of its $USD value over the last 6 months (which is the market that the liquidity pod has been working in).

If we work in $ETH terms, and use MVI as a proxy, then MVI has lost 31% vs ETH, so a 50:50 (cold wallet HODL) portfolio would be down 15% in ETH terms over 6 months.

AUM allocated

Coupled with the large AUM needed for DEX liquidity ($5 M of MVI:ETH would give a 1% price impact trade ~$25,000. [with another 0.3% LP fee for the trader]).

- $5 M of assets losing 30 to 50% in USD over 6 months is painful.

- 1,156 ETH of assets ($5 M 180 days ago) losing 13% is also painful (~150 ETH lost on the MVI + ETH HODL).

Impermanence loss

Token pairs on xy=k constant product DEX (uni v2 etc) also suffer IL. However, it’s not as big a deal as some think. An x2 price divergence results in a 5.3% loss vs HODL.

For the MVI ETH case above a 31% drop of MVI vs ETH creates a 1.7% IL.

So, If you LP’ed $1,000,000 MVI ETH on uni v2 for the last 180 days you would have lost:

- 16% due to ETH price action (-$160,000)

- 27% due to MVI price action (-$270,000)

- An additional 1.7% due to IL (-$17,000)

- Total = -44.7% (-$447,000)

Note: You would have earnt some LP fees.

If the bear market had been reversed, then the IL loss would still happen, but the price gains would drown it out.

The key point for indexcoop:

For a constant product DEX (xy=k), IL is not great, but price action dominates liquidity pod PnL.

One other point is the ILis only crystalised when you exit the position, if MVI gains vs ETH in the future, then a passive LP position will see IL reduce.

Concentrated liquidity

Concentrated liquidity is great because it lowers the AUM needed to give a specific market depth. $100,000 of liquidity can have the same trade experience as $1,000,000 of xy=k.

However, IMHO it has three downsides:

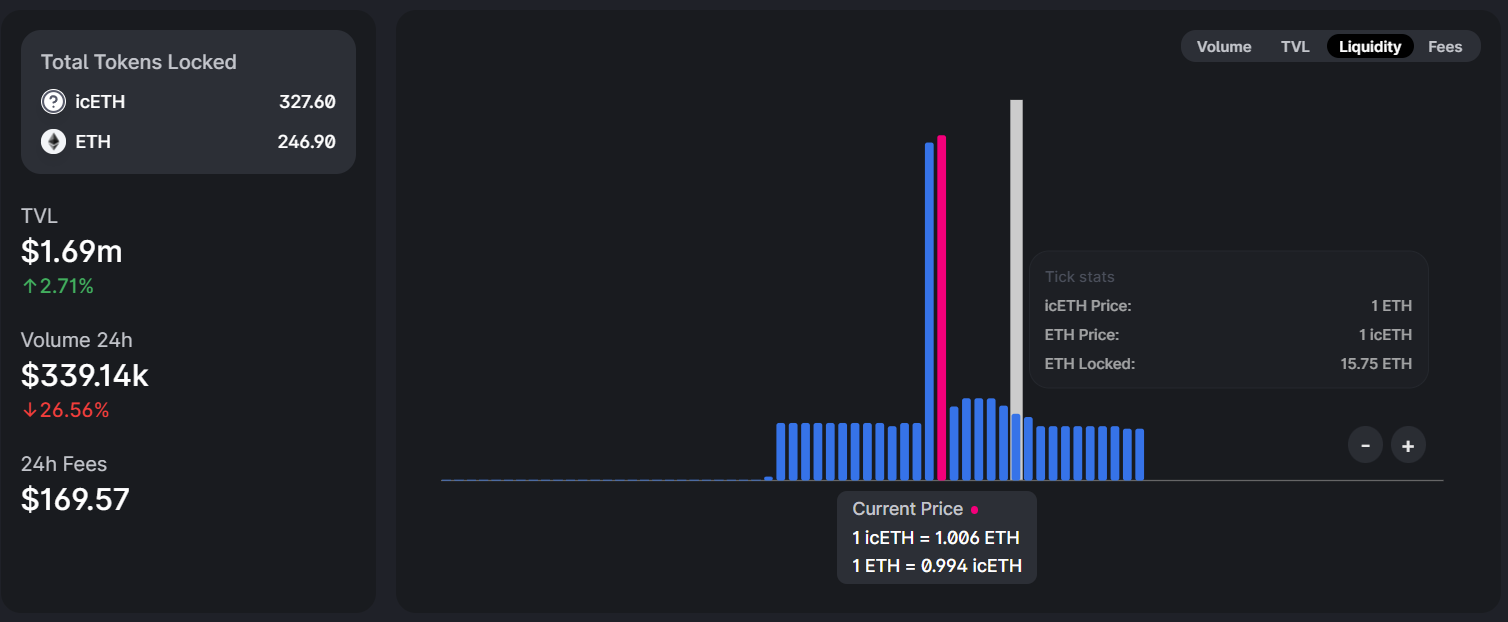

- v3 LP’ing is a competitive game, a more concentrated and active LP will capture an above-average share of fees (see the Big Friendly Whale in the icETH pool below).

- Active management costs attention and Gas

- Or use of a 3rd party manager service with smart contract risk / fees.

- Note managers take a share of the fees, but suffer no IL.

- Or use of a 3rd party manager service with smart contract risk / fees.

- Concentrated positions concentrate the IL. So if the prices diverge over time, the LP has to sell the underperforming asset to buy the other (sell low buy high).

- This works both ways: if a pair diverge 30% and then reverts to the original ratio.

- The V2 position has zero IL.

- The active v3 position has crystallised some IL each time they reposition (whether manual or using a manager such as G-UNI or VISR).

- This works both ways: if a pair diverge 30% and then reverts to the original ratio.

Some additional reading:

- [2111.09192] Impermanent Loss in Uniswap v3 (review of LP positions by Bancor team)

- https://thedefiant.io/uniswap-v3-impermanent-loss/ (replicating the above)

- https://medium.com/auditless/impermanent-loss-in-uniswap-v3-6c7161d3b445

- Concentrated Divergence Loss (and feel my pain

)

)

I think that my blog differs in that it looks at the costs of repositioning an LP position, I’m not sure the others tried to do this (but they are either wide all wallet reviews or a mathematical prediction)

INDEXCoop concentrated liquidity

So, by using concentrated liquidity, we save capital, and so reduce the total $ value loss in a bear market. However, the IL may well be higher % relative to $ deployed (and possibly higher in $ terms than if we had much more AUM in a constant ratio pool).

I suppose you could consider concentrated liquidity as leveraged liquidity, more depth = more exposure to fee income. There is no risk of liquidation. However, forced periodic rebalancing will bleed NAV decay just like a FLI product (an analogy that probably only works for 6 people in the world…).

Note for Yielding products paired with their parent token, then the divergence should be predictable and one direction so it becomes easier (I’ll be writing a blog on my icETH positions).

Obligatory Bancor comment (![]() )

)

For a protocols governance token, depositing their native (i.e. $INDEX) treasury tokens into Bancor effectively solves POL:

- Uses idle treasury tokens

- Provides liquidity

- No need to buy other token ($ETH) so can be deep at little cost to the protocol.

- No IL

- Fully passive

- THe impact of price movement is identical to holding in the treasury multi-sig.

However, for coop products, liquidity pod would need to buy the products, so it would have a significant capital cost (and is a constant product so needs more capital).

There is also the small point that Bancor doesn’t currently whitelist structured products like DPI. but I’m working on this. ![]()