In this post, we outline an expanded vision of the Index Cooperative - something much bigger than most of us would have initially imagined.

The opportunity for structured products is massive and the timing is now

From 2018-2020, we saw the foundational pieces of DeFi laid down. This includes borrowing/lending protocols (e.g. Compound, Aave), trading venues (e.g.Uniswap, Curve, Balancer), and asset issuance (e.g. USDC, DAI, WBTC, and governance tokens). In the coming years, we expect these foundational layers to continue to grow significantly in scale, size, and liquidity.

Significant lending and trading liquidity on this layer enables a whole new layer of new financial instruments to now be built - which include structured products (e.g. Index Coop), options/futures (e.g. Hegic, Opyn), insurance (e.g. Nexus Mutual), and fixed income/lending (e.g. Barnbridge).

Blackrock has a $100B market cap and the total market value of structured products can be estimated to be 5-10x bigger ($500B-$1T). If there is any translation into DeFi, this means there’s a significant opportunity.

Typically, index ETFs are the highest AUM, but a majority of Blackrock’s revenue comes from other sources. The DeFi Pulse Index is the product that is the tip of the spear that is expected to pierce to the broadest audience.

Structured products are broader than indices

So far the Index Coop has been about indices - a structured product most people know about. And the Index Coop has launched the DeFi Pulse Index, as its first and flagship product and is collaborating with CoinShares for a second index product.

If one takes a magnifying glass and looks at the ETP landscape in terms of volume, the landscape of products is much broader than indices. In fact, it’s just the tip of the iceberg. Other voluminous products include:

- Leveraged/Inverse Products: Products that allow users to easily get leveraged or inverse exposure without needing to deal with margin requirements or liquidation risk.

- Bond ETP: Products that allow users to get simple exposure to a portfolio of debt instruments with a targeted risk/reward profile

- Volatility Indices: Products involving futures/options that allow users to make bets on the market or sector volatility.

Given the ingenuity and composability of DeFi, there are probably numerous other products that can’t be imagined yet that will be possible.

Structured Product Roadmap

- Indices (Today): Analyzing the index opportunity landscape, there are ideas of L2, data protocol, and NFT indices but there is limited opportunity for indices outside of DeFi today that can grow to significant size ($100M+ in TVL). There are some opportunities to launch smart beta DeFi products and to collaborate with large asset managers for other unique indices (e.g. Coinshares).

- Leveraged / Inverse Tokens (2021): Many projects like dYdXand bzx have tried leveraged/inverse products, but they historically haven’t worked due to lack of secondary market access and liquidity. With Uniswap and its deep liquidity on pairs, that has changed and products such as leveraged/inverse ETPs are finally feasible (h/t @scott and DeFi Pulse for this idea).

- Bond ETPs (Late 2021/2022): As traunched debt positions are not yet live, the community today can only build relationships with up and coming providers like Barnbridge and Saffron Finance to launch debt-related ETPs when the products are mature and liquid.

- Volatility Indices (Late 2021/2022): Similar to Bond ETPs, the technologies here are early and the correct action is to build relationships with futures/options/synthetic technology providers (e.g. UMA, Opyn, Hegic) and brainstorm solutions.

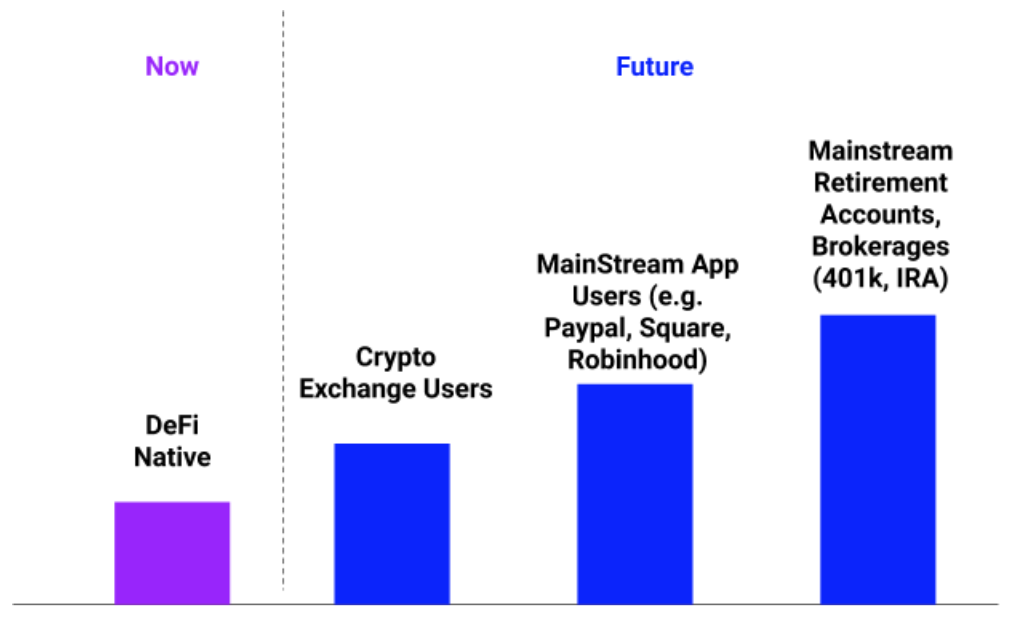

User Acquisition Progression

In terms of growing Index Coop’s structured product adoption, we can see it as a progression of dominoes - where knocking one down allows the knocking down of the next.

- DeFi Native (Today): Today, the marketing/BD has been focused on gaining market share of existing Ethereum holders (those who can use Metamask/hardware wallet) - of which we likely have 10-20% market penetration and want to grow to 60-70% (closer to lending/borrowing and exchange levels).

- Crypto Exchange Users (2021): A big part of the efforts today is getting listings on CeFi exchanges (e.g. Binance, Coinbase) - as it unlocks millions of new users who can access Index Coop’s products.

- MainStream Users (2022): Once on crypto exchanges, the next step is to get on mainstream web2 financial applications like Robinhood, Square, and Paypal - unlocking more users.

- Mainstream Exchanges and 401k (2023+): In the next 5-10 years, it can be imagined that people can get Index Coop products on the NYSE, Nasdaq, and via retirement accounts.

Launching new products and DPI as the spearhead

Up until now, the Index Coop has focused on growing the DeFi Pulse Index - with the current view that it is better to get a single index to scale first then launch additional indices. The DPI is expected to be the spearhead / flagship IndexCoop product in which most retail users gain exposure to Index Coop offerings. Once users have learned about the DPI, there will be a plethora of other products that they can adopt and follow up with. Although most of our marketing/BD focus should initially be on the DPI, the vision is to have a range of products that Index Coop users can choose from.

The Index Coop can only truly be successful with a suite of useful and widely adopted products and the DeFi Pulse is just the tip of the iceberg.

Existing leveraged inverse ETP use futures/options to keep the roll forward mechanisms and liquidity going, and there’s usually slippage in form of backwardation/contango for the holders.

Existing leveraged inverse ETP use futures/options to keep the roll forward mechanisms and liquidity going, and there’s usually slippage in form of backwardation/contango for the holders.

-TGT

-TGT