Extend INDEX liquidity mining incentives for the DeFi Pulse Index (DPI) Set for 30 days with a lower (35% reduction) issuance rate.

Abstract

Create a new INDEX liquidity mining program for the DeFi Pulse Index Set with the following parameters:

Programme runs for 30 days (from ~12PM PDT, January 6th 2021 to ~12PM PDT, 5th February 2021).

Programme will use the same staking contract as IIP-11 to remove the need to unstake and restake.

Programme will have reduced issuance rate (2,500 vs 3,864) compared to IIP-1 (a 35% reduction)

75,000 INDEX represents 0.75% of total issuance and about 1.5$ of the unallocated issuance.

Motivation

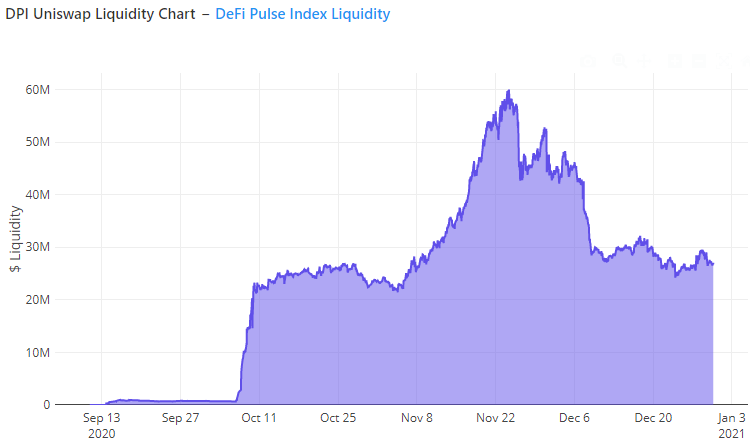

The DeFi Pulse Index currently has high liquidity on the Uniswap ETH - DPI pool. This is in part due to the liquidity mining incentive program. High Uniswap liquidity allows users and third party integrators to confidently enter and exit DPI positions.

The current liquidity mining incentive program ends on January 7th. This proposal seeks to extend liquidity mining incentives with a new liquidity mining program to continue growing distribution and adoption of the DPI.

The change from 15,000 INDEX to 3,864 per day was accompanied by a significant drop in liquidity in UNSIWAP in early December:

Work is ongoing to activate intrinsic productivity contracts to capture more income from DPI (which may be used to incentivise the liquidity pool). This will not be available until February

In addition work is ongoing to allow easier access to exchange issue and redemption for large purchasers. Again, this is unlikely to be available until February.

FOR

Extend liquidity mining incentives for the DPI set according to the parameters above.

AGAINST

Do not extend liquidity mining incentives for the DPI set according to the parameters above.

Specification

Overview

The deployed smart contract being used for the current liquidity mining program can be extended, but only for the same timer period.

The proposed smart contract for distributing liquidity mining rewards functions exactly the same way as the current liquidity mining smart contract:

Existing stakers need to take no action.

New stakers would need to:

Users deposit ETH and DPI into the Uniswap ETH - DPI pool and receive Uniswap ETH DPI LP tokens.

Users deposit their Uniswap ETH DPI LP tokens into the proposed Index Coop liquidity mining contract.

Users receive INDEX tokens in proportion to the quantity of ETH DPI LP tokens deposited.

Extend DPI liquidity Mining on Uniswap for 30 days at 2,500 INDEX per day

Voted in favour. This proposal stays true to what we agreed, which was to adjust rewards to target adequate liquidity in Uniswap, it’s also great news that users don’t have to re-stake this time!

The work being done on retention analysis will give us even better data to fine tune rewards in future, and hopefully help continue to grow the outright number of DPI holders.

In the meantime with Sushi including DPI in their Onsen, it seems using 1inch for larger trades is the way to go for now.

I think you guys are thinking about this backwards. You keep trying to reduce the incentives I believe this will ultimately have a negative effect on the protocol.

These incentives should seek to ingrain DPI LPs into the Index community. By choking off paths to community involvement via reduced issuance you risk stifling the community in its infancy ultimately hurting its long term growth.

By reducing issuance you make LPing for DPI transactional which is exactly what you don’t want. You want to build a community. Giving away more tokens than less will help achieve that.

It’s like the phrase "own 1 Bitcoin and it’s worth $33k, own 21 million and it’s worth 0.

I already think the initial distribution was too centralized. I believe the Index community would benefit from promoting more involvement in the early stages rather than causing this number to shrink by having potential LPs find better opportunities elsewhere.

I tend to agree with this point. Focusing on LPs needs to be a huge effort. We consistently see that the protocols that are most profitable for LPs are the ones that attract and maintain the largest shares of capital. For example Badger DAO.

DPI-ETH should be a top-ten pair on every exchange. The economics of market matching exposure for LPs make a ton of sense. We just need to help the LPs see that. Obviously is the hard part - but I think we are well on our way.

I think the “maintain” part is the much harder question. We don’t want to attract too much mercenary capital which all these incredibly high APY pools end up doing.

I disagree with @Lauracroft213 here because judging by the analytics board, most of the APY goes to a few miners that would have no interest in joining or actively participating in the community anyways.

I don’t see how low vs high APY affects a relationship being transactional or not. Intuitively, it almost feels like high APY would be more transactional.

We do want to increase distribution and have plans to give out more tokens to the community - that would be preferable to liquidity providers if it can be helped.

This is obviously going to pass by a large margin, and is probably a good way to keep liquidity in the UNI-pool high, but as an LP since version 1 of the incentive scheme, I can add that my biggest hang-up is being unsure what to do with the $INDEX received.

I’ve read several forum discussions on this topic, but it’s not yet clear to me what the goal is for holding. I wonder if other LPs have the same conundrum…

this is a good point. I’ve been selling half of the INDEX received and keeping the other half. I’m actually not sure what the INDEX governance allows? Would it be possible to have a vote to by-pass the DPI criteria and force adding SUSHI to DPI?

Im not sure I agree higher APY is more transactional.

I also think you risk losing a lot of benefits of rewards in the first place. For example, the Sushi ETH/DPI pool now rewards more than the Uniswap pool.

At that point, you risk fracturing the liquidity which from a purely selfish protocol perspective is actually bad. That’s ignoring the game theory and behavioural econ of creating a community, creating actual loyalty, and incentive alignment around token distribution.

A big reason Ethereum is successful is not because people like it more, it’s because they hold big bags of it, and thus they are incentivized to try and make it work and ignore competing protocols. The same goes for Index.

If you want a lot of people to love Index, make it worth their while, give them a real stake in the protocol.

Why? Lower APY is not affecting the liquidity or TVL of DPI. Instead of incentivising LPs (and I’m one of them), wide distribution of $INDEX should be achieved through contributor rewards, things like the upcoming Dharma partnership and other growth & marketing initiatives coming out of the GWG.

We don;t get to decide the APY, we provide the INDEX tokens as incentive, then the market decides how much liquidity to add to the pool and stake. It looks like the market has settled about 25%.

At the moment I think the INDEX liquidity mining is driven by iniertia.

There isn’t a great deal of divergence loss between ETH and DPI, and no action was required at the start of Jan to stake and unstake. So most probably just let it ride.

If we decide to continue after the start of Feb, I would be thinking of reducing the number of INDEX issued each day.

We want distribution of INDEX, and we want a large liquidity pool (reduces slippage, allows arbitrage at lower deviations from NAV, and gives larger holders confidence they can exit whenever required).

Over 50% of DPI is outside our incentivised pool, this is the goal as otherwise the coop is -ve cashflow.

Another question which was raised somewhere else, why do we incentive uniswap? And no other platforms? What does uniswap do for index coop?

Maybe I saw this discussion over at PieDAO. They have some nice discussions, too.

Given the fees are equal, a rational market would likely trade on the largest pool. This is true for DPI, but most INDEX trade is on Uni while the liquidity is on sushi.

The only explanation is that more people need to use Dex aggregators.