Still a strong proponent of considering separating the yielding asset from the base one. We defiantly should have some intrinsic yield, but it should be opt-in. We shouldn’t be shooting ourselves in the foot by adding additional legal concerns and possibly jeopardizing the exchange listing of DPI by adding yield to the base product by default.

4 Likes

@Kiba really happy that you are leading this up. I have tremendous confidence that you are the best owner who can drive to a solution and solve this problem once and for all. I’m glad @Thomas_Hepner summarized the steps we need to take to break this logjam.

In my opinion either having a seperate yield bearing DPI or giving people the ability to stake their DPI is the best option. This will keep our existing product whole, provide an awesome new product, and eliminate some of the concerns around meta-governance.

This needs to happen and this needs to happen soon. If we have a product launched with intrinsic productivity by the end of May- we are winning. If not our competitors will continue to yap at our heels. Let’s throw some energy behind this and make it happen!

4 Likes

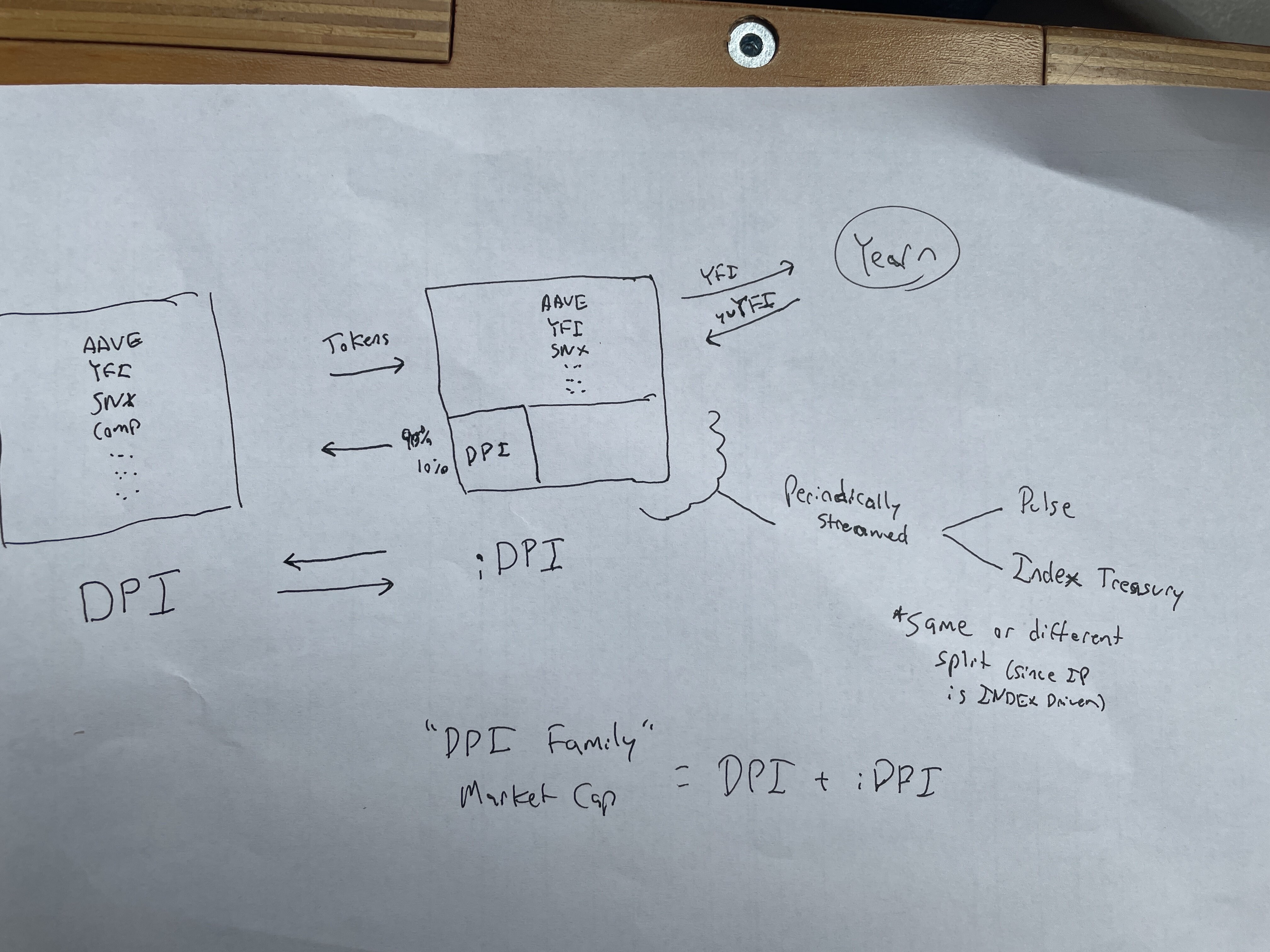

Reposting now that it is a bit more thought out and after speaking with more members + Pulse, also with a diagram in case there are other visual learners like myself (I apologize for the bad handwriting).

Goal: Keep the main DPI product vanilla, regulator/CEX exchange safe, while providing the more adventurous a way to benefit from the intrinsic productivity in the DPI assets.

Sub-goals: Make a repeatable process for other IndexCoop Products (MVI etc). Empower INDEX holders to decide the balance of return vs. metagoverance power, allow the IndexCoop to make DeFi partnerships to externalize yield decisions (Yearn, Harvest, etc).

Proposal: create a vault controlled by IndexCoop (temp name: iDPI) that allows the deposit of DPI for iDPI, and redemption of iDPI for original DPI deposit, plus yield (in DPI).

This vault will keep a percentage of deposits in DPI to handle redemptions (10% using the number from above). The other 90% will be unwrapped into their components, which will be put to work (ex: YFI → yvYFI).

As for the streaming fee. The 10% that is held in DPI is already handled by the existing DPI streaming fee. As for the remaining 90% that is put out to farm, a portion is periodically streamed (same percentage) to Pulse/IndexCoop. This has the added benefit of diversifying the treasury should we take the streaming in its unwrapped form. The split can be the same or changed since INDEX is running the vault.

Lastly, as for Market Cap, this obviously complicates the calculation. Proposing a new metric, “DPI Family Market Cap” (DPI Market Cap + iDPI Market Cap)

A few benefits I want to stress:

- Regulator/CEX friendly. “vanilla” DPI isn’t touched. If yield is allowed in your jurisdiction you can opt-in.

- Added risk of the yield is taken on only by those seeking yield (opt-in).

- Very beneficial for the IndexCoop, the ability to seek out partnerships with the vaults, and a way to diversify treasury.

- Repeatable Strategy for future products (engineering effort hopefully is high upfront cost once, and can be deployed for MVI or other future products)

more than happy to work with @Kiba or anyone else working on this. would love to see something built so we can cut off this line of attack on our product without jeopardizing the nice simple investor-friendly vanilla nature of DPI.

7 Likes

Great discussion so far! Wanted to present a summary of the conversations above and a general framework we can use to evaluate this opportunity.

This framework lays out some of the considerations from the discussion above into context around advancing core metrics, timing and implementation strategy:

Some notes:

- There is insufficient evidence that IP will lead to TVL growth, but will 2-3x Coop revenue from the DPI as Kiba mentioned above

- At the same time, there are differing opinions from the community on implementation strategy which makes this a high risk initiative

- In terms of timing, there are pending extrinsic productivity integrations (AAVE, sDPI), CEX listings, additional rebalance operations (unwrapping prior to every DPI rebalance) which also adds significant complexity other than engineering.

- Other product launches in the horizon that serve different use cases may be a better testing ground for IP i.e. BED and Synthetix Debt Mirror Index

A path forward could be aggressively pursuing IP in the Synthetix product which serves a different audience and use case. We use the data collected to inform us on IP in DPI as more integrations come online and implementation strategy becomes clearer

6 Likes

A couple of points from me mostly on the revenue potential.

In @Kiba’s proposal, it says that:

Yet, @richard’s post says that revenue growth for the Coop could be significant while TVL growth from this is uncertain.

Would be great to clarify how we are actually thinking about this.

Assuming revenue is split in some way between Coop, DeFi Pulse and DPI holders - what is the true revenue potential for the Coop? Also, what do those revenue numbers look like assuming 50% of all DPI locked in the vault? What if it’s 30%?

I think it’s rather crucial that we understand what these numbers look like. Something that is worth doing for 2-3x in revenue might not be for 0.5x. At least it wouldn’t be a high priority.

In terms of the execution of intrinsic productivity, the proposed option with the vault makes the most sense to me as it 1) doesn’t affect integrations; 2) doesn’t affect CEX listings; 3) doesn’t farm the underlying assets without consent. But like I said above, it will reduce the revenue impact.

Pursuing IP with the Synthetix product seems like a better option.

While we are on the subject, I wanted to briefly touch on IP for MVI and just give everyone some context here.

At the moment, only one token, $DG, can be staked in governance. Governance yield on $DG is 40% and there’s a proposal to extend rewards at the current level for the next 10 weeks (original target was 20%). $DG is about 5% of the index. We know that both, AXS (7% of MVI) and SAND (10%) will enable staking when they migrate to their own sidechain in the case of the former and when the game goes live in the case of the latter. ENJ (17%) could also be staked in the future when their Polka parachain is ready to go.

In terms of experimenting on a small scale (MVI is currently at $5m TVL), MVI could be interesting. The revenue on $DG alone would be 2%. As Index Coop is the methodologist here, any revenue will be split between the Coop and MVI holders.

7 Likes

I just want to mention that bDPI from BasketDAO may be some level of proof of the desire for IP. I know they are supplementing with BASK rewards too, but they have grown bDPI to ~$60m market cap. Seems like the immediate growth potential for IP with DPI is somewhere between $10m-$30m (just my estimate). Future growth is harder to determine.

I like the thoughts proposed by @oneski22 around keeping vanilla DPI and having a second product, iDPI.

Imo, the most important thing is that we get moving with intrinsic productivity - as @BigSky7 said, competitors are yapping at our heals here. If we are constrained by ENG resources, it probably makes more sense to start with SMI for intrinsic productivity and lean outwards from there. We are going to do it there no matter what, so let’s take that head on.

1 Like

Could be interesting to make intrinsic productivity opt in - this would potentially solve for concerns from integrators (exchanges, lenders, etc) about risk and pace of product changes, while allowing users and the Coop to benefit from yield as desired.

So you could have xDPI, which represents the same underlying assets and weights of the DPI index but includes intrinsic productivity strategies where available. Users could trade it, do the regular creation/redemption for underlying assets, and potentially the Coop could create pools for migrating between DPI and xDPI and handle the unwrapping/wrapping in batches.

2 Likes

Personally, I’m much more in favour of kicking off intrinsic productivity on MVI first:

- Compared to most underlying tokens in DPI there are higher yields available on wBTC, ETH and DAI even if just using a simple Compound strategy (yYFI is currently yielding < 3%).

- No external integrations / CEX listings.

- While the rebalances are more frequent, they are likely to be much simpler (and the rebalances are the hard part).

When we implement Intrinsic productivity for DPI (it is inevitable  ), I would argue for all the income to goto INDEXcoop and we can decide how to allocate that income (offsetting streaming fees down to zero, liquidity mining DPI…).

), I would argue for all the income to goto INDEXcoop and we can decide how to allocate that income (offsetting streaming fees down to zero, liquidity mining DPI…).

I don’t like staking for income as it prevents the holder from using the token for other uses and it adds more contract to be deployed and maintained. Also, until we get L2 staking, it becomes a gas drain for smaller stakers.

Creating a xDPI is possible (whether we have sufficient AUM to split it), but it would be an additional product to launch and integrate with the rest of DeFI.

2 Likes

You mean SDI right, not MVI?

2 Likes

On SMI IP

Majority of this discussion have been about our strategy specifically for DPI. Since they are different products/audiences there are many independent considerations for each. Even if we do SMI IP first, we will still have to circle back to this same conversation for DPI anyway. Also SMI doesn’t exist yet and might be months away.

There isn’t any material difference between DPI and SMI besides that DPI is already established and we have set a precedent for it to not have IP. Besides some small technical differences for integrators like calculating NAV it doesn’t meaningfully change the product in anyway, its just a perceptual change of DPI vs stkDPI where as SMI doesnt have that cognitive shift because we want to do IP from day one. If you’re invested in DPI you are already accepting a huge amount of risk (regulatory, financial, smart contract, and counterparty risks at the very least) while adding IP only increases smart contract risk by a fraction compared to base DPI, especially since this IIPs proposed strategies use protocols DPI holders are already invested in.

Opt-In DPI w/ IP

Opt-in solution is the unanimous preference from everyone on this thread and who I talked with around the DAO this week. Main objective of this is to isolate risk to help with integrations and BD with institutional investors. Personally I would prefer keeping it all within DPI but not opposed to second product if that’s what everyone wants.

Set can provide better advice than me but from what I can tell the best way to implement this is as a second Set token independent from current DPI. It will follow same methodology, have same streaming fee and cut to DFP/IC, but will have IP implemented in it. We use both Set tokens to calculate TVL of DPI. Farming mechanics would be as described in this IIP.

A second product is simpler than the vault idea from @oneski22 since there’s no real reason to have stkDPI and DPI tightly coupled like that. They are loosely coupled by methodology and the market can figure out pricing between the two.

There’s only one DeF integration that we currently have that would require updates with a second product which is CREAM and I help set it up so not a big deal getting it done again. The point of second product is to keep DPI vanilla and make ongoing integrations easier so saying “second product is more work” is a direct consequence of “keep DPI vanilla”.

From reading the docs on rebalance contract it seems to me it’s possible to keep xSUSHI and yvYFI in the set during rebalance by including their current token balances in _oldComponentsTargetUnits. With the parameters for farming in this IIP, 10% of component in DPI is enough to cover any rebalance and if a component’s allocation is reduced to <10% is liquid after rebalance then the farming managers / keep3rs rebalance back to 10%. What am i missing @richard that makes unwrapping mandatory before rebalances?

I agree with others that we should be focusing on growth and our users instead of revenue. I included revenue to IC in original post to avoid giving profit to DPI holders and making it a security. While there is no direct lever to growth, the additional yields make it a more attractive product (re: BasketDAO) and we earn our fees in DPI so an increase in TVL + increase value of DPI increases our income while still focusing on growth. It also opens us to a more DeFi aware audience since many can currently outperform DPI with yield farming but it would be harder to outperform DPI + IP.

There’s obviously a lot of duplicate convos happening p2p between Coop members on this IIP so Greg/Dylan/Punia are helping me setup a small workshop / group to hammer out details with a small group of people.

4 Likes

Since the snapshot cannot be updated, posting here: the 20% APY for YFI is no longer accurate, the actual number is below 1%. Here is a link to see the live 30-day average APY directly from yearn.

[Grafana](https://Link to Yearn.Vision Dashboard)

0.718% or so is the current APY, the quote on the main yearn website is 1.09% Gross, 0.88% net.

This drastically changes the projected revenue of this change.

3 Likes

There’s a lot been said here and I have a lost a clear view. I entirely accept that can be my problem and that I probably just need to DMOR. There’s a lot of knowledge here though and if I have questions maybe others do too:

I am mega FOR intrinsic productivity, it seems like leaving money on the table otherwise, at least being inefficient. And, it is essential for competitiveness.

BUT

The methodology from DeFi Pulse says use the bearer instrument …yet @scott_lew_is seems for.

great post kiba.

i would suggest being more aggressive than 75%.

That’s cool and provides strong motivation to support it. Is the proposal possible because DPI is minted according to the methodology but then the tokens swapped out by the IC? Wouldn’t that still affect CEX listings and institutional purchases? Furthermore, @reganbozman fully supports the proposal, but he does qualify it by saying

‘we should do a legal analysis of this but I don’t see a strong reason to not implement this barring that’

Regan’s opinion counts for a lot and his suggestion seems reasonable but there is no explicit legal analysis following.

It says 20% for Yearn but then that is corrected to less than 1% in a comment:

0.718% or so is the current APY, the quote on the main yearn website is 1.09% Gross, 0.88% net.

…that seems a big change without commentary. Not including aSNX was based on it having a rate lower than 2%, so should YFI be taken out too? Is it worth the engineering time and risk if the return has become so low?

The yvYFI vault had a flaw. Lightning rarely strikes twice but opening up the prime Coop product like this is not just about voting for increased productivity, there’s fundamental change to the risk profile.

Considering the above, despite the desire to be quick, it is hard to cast a vote even though the overall aim and initiative is right.

2 Likes