Summary

Authors: @JosephKnecht, @MrMadila, @anthonyb.eth, @ElliottWatts , @PrairieFi, @afromac, @Don-ETH, @sidhemraj, @LemonadeAlpha, @DocHabanero,

To help achieve one of Products Season 1 objectives to ‘Build a portfolio of sustainable products’ we have launched the Product Profitability Initiative.

One of the KPIs outlined in the Season 1 for the product team is to launch products with at least a 70% contribution market. In order to achieve this objective we had to understand how our current products have performed and how we can reduce cost.

Abstract

Put bluntly, the index products are profoundly unprofitable.This is due to the very high costs of liquidity mining incentives (LMI) and rebalancing. For example, as you can see from these Dune analytics dashboards, both BED and DATA are deeply unprofitable even when excluding liquidity mining incentive (LMI) costs.

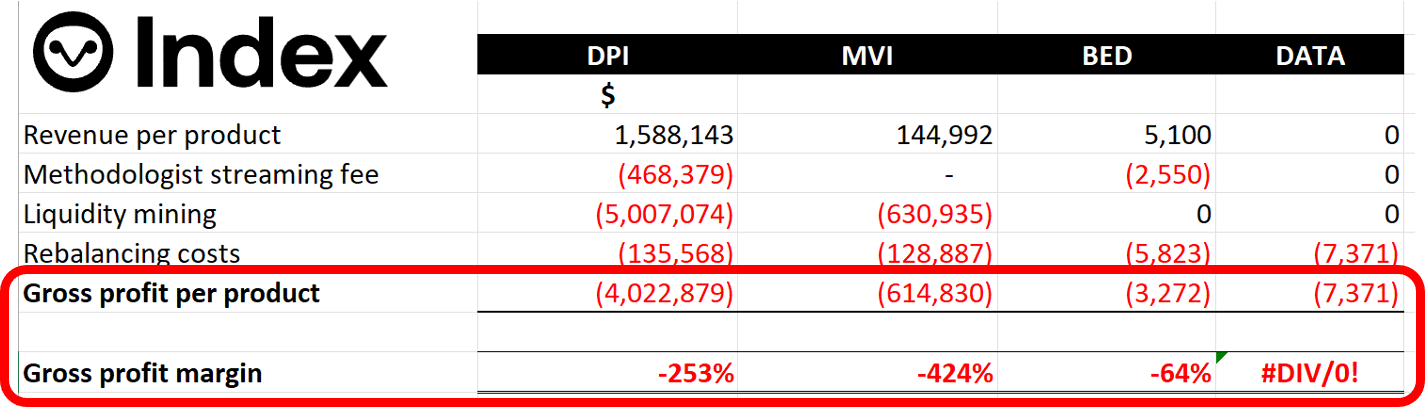

Similarly, here are the year to date gross profits for DPI, MVI, BED, and DATA including LMI and gas costs where available.

As you can see, the products are deeply loss-making. These only consider gross costs and do not include operational costs such as contributor and marketing expenses. The very heavy losses of our index products have come into sharper focus recently because of the Coop taking on the gas costs from Set.

You might ask, ‘But surely as AUM grows our products become more profitable, right?’ The answer is, ‘No’. This is a very widespread misunderstanding. If the products are unprofitable then scaling will only cause us to lose more money more quickly. This is because both the income and rebalancing costs scale approximately with NAV for fixed tradesizes. We need to fix the unit economics of our products before we can effectively scale.

To achieve this, here are the next steps we will be taking.

NEXT STEPS

Product

- Severely curtail rebalancing for future products. For future proposals on Layer 1, ‘no rebalancing’ (with the exception of allocation caps) will be the default. Any products which propose rebalancing will need to make a strong case why rebalancing will improve profitability. By ‘rebalancing’ we mean adjusting the allocations to match a target allocation. This is distinct from recomposition, i.e., adding and removing components, which we address below. Rebalancing has very weak financial justification and is our largest product cost alongside LMI. Also, Set spends an enormous amount of engineering effort on rebalancing, which is time that could be better spent adding new capabilities. Additionally, rebalancing causes the assets in the index to decay due to price impact and LP fees incurred from trading. The asset decay is significant and can be 2-5% per year. We’re mindful that some customers coming from TradFi index investing may expect rebalancing but there’s no justification for it, particularly considering how costly it is for both ourselves and our customers in the form of, respectively, gas costs and asset decay. The recent rebalancing blockages for both DPI and MVI highlight this issue.

- Manage recomposition costs. Recomposition refers to adding or removing tokens to/from an index after the product has been launched. Recomposition is extremely expensive because an entire position has to be created or unwound. Further, recomposition is more expensive than adding a token at launch since we can use order aggregation and non-standard DEXs for exchange issuance but not for recomposition post launch. Also, it’s much less expensive to add a token to a $3M AUM product at issuance than a $300M AUM product a year post launch. To control the costs of recomposition, we recommend that additions/removals only take place after a waiting period and then added/removed incrementally. For example, ‘components will be added/removed after a 30-day waiting period and then only in 5%/month increments’.

- Revisit rebalancing for current products. We will work with methodologists to see what charges they’re comfortable with in order to improve profitability.

- Be gross profitable at launch. Proposals will have to include a section on Product Economics and only projects with a high gross profit margin at launch will be recommended for DG2 posting. Gross profit margin will be defined in terms of streaming and mint/redeem fees and rebalancing gas costs but exclude LMI. Although LMI is extraordinarily expensive, we exclude it from the definition of gross profit since it is considered a short-lived operational expense.

- Shorten the time to break-even. Decision Gate 2 proposals will include a financial forecast with a predicted time horizon to profitability and break-even including LMI. PWG will own the forecast but it will be reviewed by F.Nest.

- Set our prices better for maximizing profit. All DG2 product proposals will include market research on price sensitivity in order to set the optimal streaming fee. Setting prices is one of the most important decisions a start-up can make and we need to be much more intentional about setting prices to maximize profit. The product team will take on an initiative to come up with a thorough pricing strategy. This could include working with external firms to speed up and improve the process.

- Standardize. The above changes will be implemented in the next version of the New Product Proposal Template.

- Increase launch AUM. If we can make our new products profitable from the start, we then need to focus on getting larger AUMs at launch. It’s simply not economical anymore to launch a product with $2M AUM and 200 holders using funds primarily raised from Coop members. Working with EWG, we will be rolling out pre-sale fundraising pools, similar to PieDAO ovens or minting pools, in order to raise seed capital from the broader market. This is analogous to the community fundraising we have done in the past except now we will be raising from the broader market. One major advantage of this approach is that the gas costs for minting will be socialized across users, making minting our product tokens far less expensive. More details on these pre-sale pools will follow.

- Retire unprofitable products. We will retire products which are not profitable nor have any prospects of becoming so. This will need to take into account the considerations of the Methodologist. We will describe this process in a follow-up post.

- Standardize. We recommend that the WTA assessment consider gross profitability alongside revenue potential and operational cost. The current WTA assessment splits revenue and cost which makes it difficult to assess if the products being put forward will be profitable.

- Prioritize Layer 2. In order to reduce acquisition costs for our customers, all products will also be launched on Layer 2 unless there is a strong case not to. We recognize that native deployment on Layer 2 is currently hampered by the lack of tokens and liquidity.

Liquidity

- Optimize and control LMI costs. Liquidity mining incentives will be used more optimally according to the Harmonic Liquidity process.

Analytics

- Report profitability. Gross profit for the products will be included in the analytics dashboards and the weekly stand-up reporting. Additionally, we will provide dashboards for asset decay. Tracking asset decay is an important counterbalance to prevent Product Designers from pushing rebalancing costs onto our customers in the form of higher trade sizes and thus higher asset decay.

- Understand what factors drive product inflows and outflows. Net inflows is a NorthStar metric but we know surprisingly little about which factors drive it. Specifically, we have no understanding of the relative importance of product composition, marketing, promotions, ticker symbol, product and underlying liquidity, the product designer profile, social media sentiment, fees, market conditions, competing products, launch AUM, etc. This is an extraordinarily difficult problem akin to trying to predict box office revenue for a new movie release. Analytics will begin efforts to try to predict which factors drive fund flows. Given the difficulty of the problem, we are not expecting a well-developed model anytime soon but we believe, at the very least, the framing of the problem will sharpen our thinking.

Finance

- Report profitability. Finance will provide monthly reports on the gross profit and gross profit margin broken down by project.

- Prioritize profitability. We recommend that gross profit be adopted as a North Star metric.

We see this plan as part of a larger transition within the DAO to focus on profitability and sustainability. Achieving profitability is key to ensuring the flourishing of the DAO and fulfilling our vision to make crypto investing simple and accessible. To paraphrase Cav’s saying ‘with no products, there’s no DAO’. Similarly ‘if there are no profitable products, there’s no DAO’. Please contact us if you have any questions, feedback, or concerns.