Title : November 2022 Automated Products Risk Report - Analysis of Risk to holders of Automated Indices maintained by the Index Coop community, namely icETH, ETH2x-FLI & BTC2x-FLI.

Authors : @sidhemraj

Reviewed by : @afromac @MrMadila @anthonyb.eth @0x_Dev

Preface

At Index Coop’s Product pod, we are always looking to adopt best practises around Risk Management and reporting on market factors affecting product performance. Communities at MakerDAO, Aave, Compound

have set a high example of dynamic risk parameter updates, and we want to adopt best practices wherever necessary.

Yield Products

icETH

Performance

During November, icETH outperformed ETH by 1.1%. This was driven by increased staking rewards following the merge, as well as stETH trading closer to a 1:1 conversion rate (sometimes referred to as “the peg”)

Figure 1: icETH value vs USDC & ETH

Supply Cap

The Supply Cap parameter is a global limit on the total units of icETH that can be created. Determining and gradually expanding this limit on units enables the Index Coop product team to safely increase the maximum number of units over time and ensure the product can successfully de-lever in all market conditions. Currently there are 10.5K units of icETH in circulation. This is equivalent to 70% utilization of the max Supply Cap. A further 4,000 units ($5.1M USD at today’s prices) of icETH can be minted before the Supply Cap would need to be raised. 1,000+ units were issued in November, a ~10% growth month on month. If this rate of growth was sustained at this price level, Index Coop will need to update the supply cap by the end of March.

Parameter updates

No parameter updates were made in November, but we anticipate executing an update to the Supply Cap in the coming months. Current circulating supply of icETH is ~70% of the Supply Cap. Index Coop aims to review and increase the supply cap once circulating supply approaches ~80%.

Figure 2: icETH Unit Supply & Supply Cap

Rebalances

No rebalances were triggered by icETH’s Aave Leverage Strategy Contract.

Underlying Liquidity

The stETH:ETH price has experienced sell pressure following the collapse of FTX. During November, the stETH:ETH price ranged from 0.95 to 1.02, with the standard deviation of 0.003. Notably, liquidity on the Curve stETH:ETH pool decreased by 60%, falling from $1.9B to $750M. As this is the primary pool used to rebalance the product, Index Coop will be monitoring the situation carefully.

Figure 3: stETH:ETH price

Aave markets rely on ChainLink price feed aggregators to function securely, so monitoring Chainlink’s stETH:ETH Price feed helps inform product parameter updates like leverage ratio bounds. Higher volatility in the stETH:ETH price feed increases chances of triggering a rebalance on icETH as the leverage ratio falls out of the acceptable bounds.

DEX liquidity

Most icETH DEX trades in November were below $50K, with an average price impact of this size trade of below 30 basis points. From another perspective, the average trade size on the Uniswap Pool during November was 13 icETH units, with an average of 0.28% price impact at this trade size.

The chart below shows the relationship between Trade Sizes and Price Impact on the pool. The blue dots above the line represent price impact for a trade to buy icETH, while the dots below the line represent trades to the pool to sell icETH back to the pool.

Figure 4: Price Impact on the icETH:ETH Uni V3 Pool

The NAV vs DEX premium

The below chart compares icETH DEX price with the Net Asset Value (NAV) in terms of ETH. The icETH price on the Uniswap V3 pool has been closely tracking NAV; the highest percentage premium during November was 0.55%, and the average premium (incl swap fee) was 0.11%.

Figure 5: icETH Net Asset Value vs DEX Price

The below histogram shows a distribution for the amount of time the icETH price traded at various Premium/Discount intervals. A positive number indicates a premium over Net Asset Value (NAV), while a negative number indicates a discount.

Figure 6: icETH time spent at a premium or discount to Net Asset Value

Aave Params

WETH Market parameters, proposed changes & forum discussion

The Aave community is planning to accelerate V3 adoption by halting new listings. As icETH borrows from Aave V2 ETH market, this would have a major impact on icETH. We will monitor the developments closely to support the product.

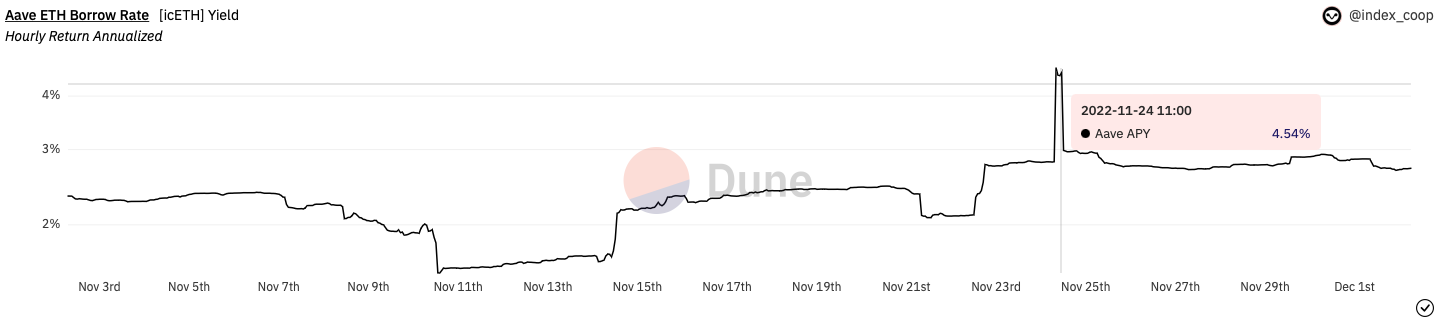

Borrow Rates Over time

ETH borrow Rates were in the 2-3% range for most of the month, apart from a brief spike on Nov 24th due to high utilization on the ETH borrow market.

Figure 7: Aave V2 ETH Market Borrow Rate

Migration to Aave V3

Index Coop is actively researching steps to upgrade or replace icETH using Aave v3 as the underlying borrowing protocol.

Leveraged Products

ETH2x-FLI

Performance

During November, ETH dropped by 17%, while the price of ETH2x-FLI dropped by 35% over the same period. The below chart shows the performance of both assets.

Figure 8: ETH2x-FLI and ETH Price

Illustrative Benchmarking:

We can compare ETH2x-FLI performance to a simple 2x Leveraged ETH position, which experiences no volatility drift. Illustrative tracking error, as shown in the chart below, is the percentage difference in price rise and fall between the 2 positions. Due to this divergence between actual and idealized performance, the price of ETH2x-FLI outperformed a perfect 2x ETH position by 15% over a 30 day period.

Figure 9: ETH2x-FLI 30 day performance comparison to a simple 2X ETH position

Similarly, please find the linked 60 day and 90 day performance comparisons in which an ETH2x-FLI position also outperformed a simple 2xETH position by 17% in the 60 day period and 30% over a 90 day period.

Parameter Updates

During November, due to low liquidity in their respective ETH:USDC pools, both Sushiswap and UniswapV2 were removed as supported exchanges for product rebalancing. On Nov 10th 2022 the ETH price fell by over 25% within hours of the news of the FTX collapse, leading to a sharp drop in available liquidity on these exchanges. This drop in liquidity led to a missed rebalance by the product. In reaction to this, the engineering pod executed a parameter update to execute all ETH2x-FLI rebalancing on UniswapV3 going forward. After the above parameter changes, the keeper system was able to successfully execute the rebalance (for more detail: see notable events further below).

Supply Cap

The Supply Cap parameter is a global limit on the total units of ETH2x-FLI that can be created. Determining and gradually expanding this limit on units enables the Index Coop product team to safely increase the maximum number of units over time and ensure the product can successfully de-lever in all market market conditions. Currently at 1.6M units i.e., 65% utilization, another 400,000 units can be minted before the Supply Cap would need to be raised. Almost 100K units were issued in November, a ~7% growth month-on-month. At the current rate of growth, the supply cap would need to be updated at the end of March 2022.

Currently there are 1.6M units of ETH2x-FLI in circulation. This is equivalent to 65% utilization of the max Supply Cap. A further 400,000 units ($2.24M at today’s prices) of ETH2x-FLI can be minted before the Supply Cap would need to be raised. 100,000 units were issued in November, a ~7% growth month on month. If this rate of growth was sustained at this price level, Index Coop will need to update the supply cap by the end of March.

Figure 10: ETH2x-FLI Unit Supply & Supply Cap

Rebalances

Currently ETH2x-FLI currently uses the UniV3 ETH-USDC 0.05% fee pool as the sole source of liquidity to rebalance. An additional benefit to product holders as a result of this change is the greatly improved capital efficiency available on UniV3. The average Price Impact (PI + Swap Fee ) to rebalance is now less than 0.1%.

The below scatter chart shows price impact at various rebalance sizes for ETH2x-FLI. The blue dots on the bottom left of the Figure 11 indicate that rebalance trade sizes below $40k generally had a price impact per trade of between 0.3 to 0.5% on Sushiswap and Uniswap V2, with larger trades above 120K USD ranging from 0.5 to 1% price impact.

Resetting the rebalancing mechanism to target Uni V3 (Figure 12) led to a massive increase in capital efficiency, whereby trades of up to $400k were executed with a price impact of below 0.2%.

Figure 11: ETH2x-FLI rebalances & price impact on SushiSwap and Uniswap V2

Figure 12: ETH2x-FLI rebalances & price impact on Uniswap V3

The below chart shows the same data on a time-series to illustrate the improvement in efficiency since retargeting all rebalancing at Uni V3 in the parameter update.

Figure 13: ETH2x-FLI Rebalances during November 2022

Notable Events

- ETH2x-FLI was late to rebalance by several hours on 10th Nov due to high slippage on Sushi and UniV2. Sushi and UniV2 were removed as supported exchanges, and as of today the keeper system solely utilizes the UniV3 ETH-USDC pool to rebalance.

Underlying Liquidity

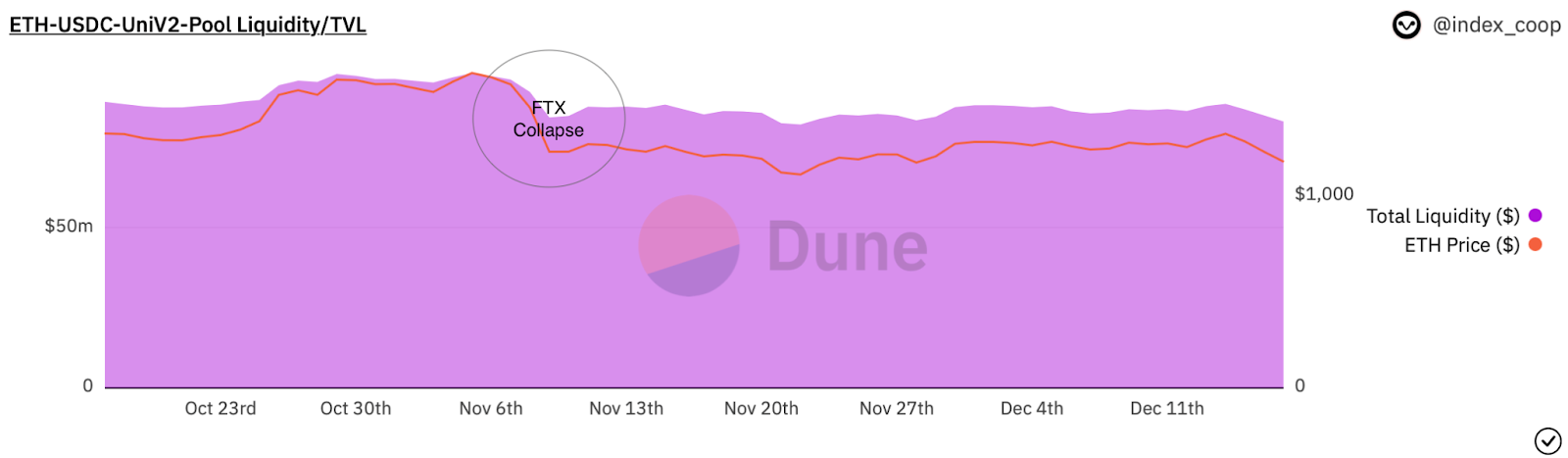

Over the course of November, each of the Sushi, UniV2, and UniV3 pools were used for rebalancing ETH2x-FLI during different periods. Total liquidity on Sushi and UniV2 ETH-USDC pools dropped by ~35% on 10th Nov contributing to the previously mentioned missed rebalance.

Figure 14: Sushiswap ETH-USDC pool Liquidity

Figure 15: Uniswap V2 ETH-USDC pool Liquidity

Going forward ETH2x-FLI will employ Uniswap V3 as the sole DEX used for rebalancing. The Index Coop product team will monitor the Sushi and Uniswap V2 pools before considering adding support for them again at a later stage if sufficient capital is available. During November, liquidity on the WETH:USDC UniV3 0.3% fee pool was sufficiently deep, with adequate liquidity distributed in a wide range. Relying on a single DEX pool for product rebalancing does introduce some idiosyncratic risk, and having a fallback option is preferable to enable product to function in all market conditions.

Figure 16: Uniswap V3 ETH:USDC Liquidity

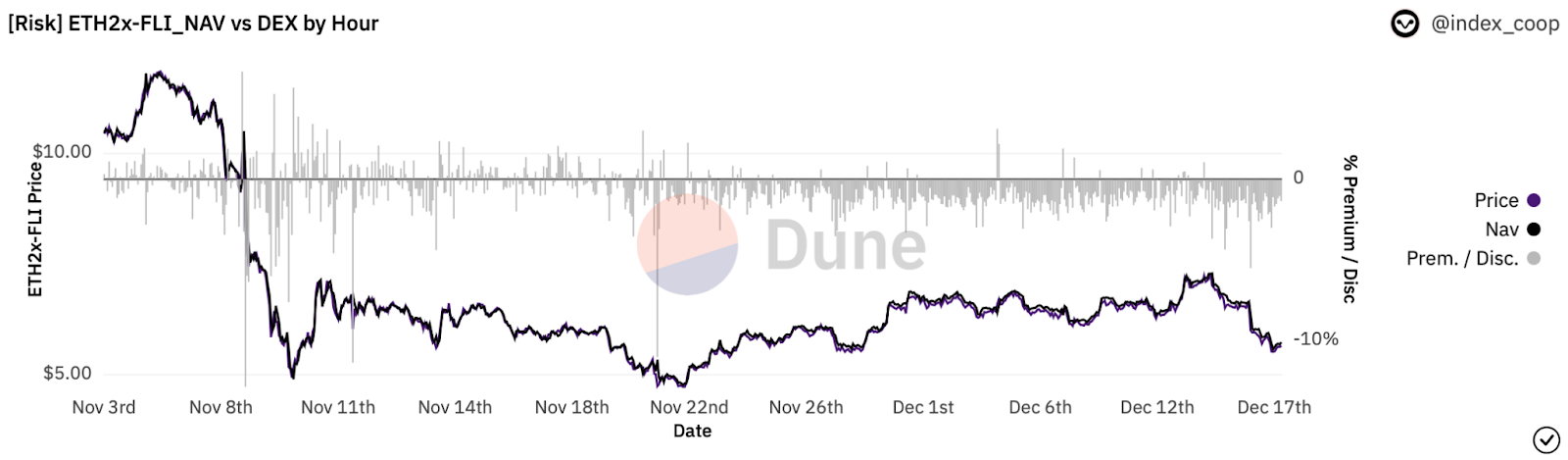

NAV vs DEX premium

The ETH2x-FLI price on DEXs tracked the Net Asset Value accurately during November for the large majority of the period. Specific instances of high price volatility around the FTX collapse coincided with notable deviation, with the product trading at both a large discount (-12%) and premium (+7%), in the time period around this event. NAV vs DEX premium hovered between -2 to 2% for most of the month, with a mean average deviation of ~1%.

Figure 17: ETH2x-FLI Net Asset Value vs DEX Price

Product Liquidity

The Uniswap V3 ETH2x-FLI:ETH 30bps pool is the dominant liquidity pool for the product, and captures 90+% of the ETH2x-FLI trade volume. On trades of up to $10,000, Price Impact incurred was between 1 and 1.3%. ETH2x-FLI buy trades have a positive price impact - indicating ETH2x-FLI price premium paid over NAV, and sell trades have a negative price impact - indicating that ETH2x-FLI sold at a discount to market price.

Figure 18: ETH2x-FLI Uni V3 Trades & Price Impact

Figure 19: ETH2x-FLI Net Asset Value vs DEX price

Compound market Parameters

ETH2x-FLI borrows from the USDC market on Compound V2, so any updates to the protocol’s parameters affects the product performance. No major updates were made to the Compound V2 USDC market in the given period.

BTC2x-FLI

Performance

BTC2x-FLI price is down 37% in dollar terms in line with a broader price drop across crypto assets.

Figure 20: BTC2x-FLI Price Performance during November 2022

Base Asset Terms

BTC price dropped 19% in the same period, with the FLI demonstrating close to perfect 2x leverage, dropping by 37% in value.

Figure 21: BTC2x-FLI vs BTC Price

Illustrative Benchmarking:

The chart below compares BTC2x-FLI performance to a simple 2x BTC leveraged position, which experiences no NAV deviation or volatility drift.

Figure 22: BTC2x-FLI 30 day performance comparison to a simple 2x BTC position

In this comparison, the price of BTC2x-FLI outperformed a simple 2xBTC leveraged position by 6% over a 30 day period, by 10% in the 60 day period, and 9% over a 90 day period. Please find the linked 60 day and 90 day performance comparisons.

Parameter updates

During November, both Sushiswap and UniswapV2 were removed as exchanges supported by BTC2x-FLI for rebalancing due to low liquidity. On Nov 10th 2022 ETH & BTC price fell by >25% within hours of the news of the FTX collapse. This led to a sharp drop in available liquidity for rebalancing on these exchanges, and ultimately to a missed rebalance by the product. Ripcord, a decentralized failsafe mechanism to encourage third parties to execute an emergency rebalance during heightened market volatility, was executed and helped the product to avoid liquidation. In reaction to this event, the engineering pod executed a parameter update to execute all BTC2x-FLI rebalancing on UniswapV3 going forward. After the above parameter changes, the keeper system was able to successfully execute the rebalance.

Rebalances

The majority of BTC2x-FLI rebalance trades were executed via the UniswapV3 BTC:USDC 0.30% pool. All rebalances had a price impact of <0.5%, apart from 1 ripcord trade which had the price impact of 1.1%. Rebalances to lever up have a positive price impact, as BTC was bought at a premium to market price, and rebalances to lever-down have a negative price impact, as BTC was sold at a discount.

Figure 23: BTC2x-FLI rebalance transactions and price impact

Figure 24: BTC2x-FLI Rebalances during November 2022

Unusual Events

Ripcord was called on 10th Nov, as regular rebalances failed due to high slippage on Sushi and UniV2.

Underlying Liquidity

TVL/Dollar value of liquidity in Sushi and UniV2 pools dropped by 30% on Nov 10th, and has not yet recovered to previous levels, as shown below in Figures 25 & 26

Figure 25: Sushiswap WBTC:WETH pool liquidity

Figure 26: Uniswap V2 WBTC:WETH pool liquidity

However, liquidity on the WBTC:WETH UniV3 0.3% fee pool has been sufficient for safe operation of the product, with plenty of depth around a wide price range.

Figure 27: Uniswap V3 WBTC:WETH pool liquidity

Supply Cap

The Supply Cap parameter is a global limit on the total units of BTC2x-FLI that can be created. Determining and gradually expanding this limit on units enables the Index Coop product team to safely increase the maximum number of units over time and ensure the product can successfully de-lever in all market market conditions.

Currently there are 381,000 units of BTC2x-FLI in circulation. This is equivalent to 38% utilization of the max Supply Cap. A further 420,000 units ($1,285,000 at today’s prices) of BTC2x-FLI can be minted before the Supply Cap would need to be raised. 50,000 units were issued in November, a ~16% growth month on month. If this rate of growth was sustained at this price level, Index Coop will need to update the supply cap by the end of July.

Figure 28: BTC2x-FLI Unit Supply and Supply Cap

NAV vs DEX Premium

BTC2x-FLI price on DEXs deviates from NAV on significantly more instances than ETH2x-FLI, with a couple of instances of extreme deviation on either side (-8% and 5%), with Average Premium/Disc being 2.14%. This NAV deviation is driven by lower trade volume and DEX liquidity, making BTC2x-FLI less economical for arbitrage bots to trade. This lower liquidity and trade volume also makes Price vs NAV visualizations harder to read at shorter time intervals. The BTC2x-FLI chart in Figure 29 visualizes these indicators by the hour instead of the minute.

Figure 29: BTC2x-FLI Net Asset Value vs DEX Price

Product Liquidity

Due to the low liquidity for BTC2x-FLI on DEXs, we recommend flash-minting BTC2x-FLI via the Index-Coop App.

Disclaimer

This report is for informational purposes only and does not constitute an offer to sell, a solici-

tation to buy, or a recommendation for any security, nor does it constitute an offer to provide

investment advisory or other services by Index Coop.